[This is the third installment of a three-part post. It may be worth reading Part 1 and Part 2 first.]

In Part 1, I began with the idea that talking about “the economy” as though it were this unitary thing can be a problem, one that was highlighted for me by recent media stories about surveys that revealed potentially counter-intuitive understanding on the part of the American public.

Part 2 focused on why it’s difficult for “the economy” to be understood consistently or effectively at either end of the communicative path that runs from national government to individual citizen. In both cases, there’s a tendency to take temporary circumstances for persistent features, and clarity tends to fall to the wayside as a result. Part of this has to do with the difficulty of negotiating scale.

Scale is a crucial part of any democracy. Political representation (e.g., the representatives that we elect on a regular basis) is fundamentally a question of scale, the idea that we, as individual voters, will have our differing interests accounted for, with some degree of fidelity, by those we elect. Rhetorically, scale is embedded in the trope of synecdoche, the substitution of part for whole. Identifying representatives by their political party and state (D - New York) is a fairly simple example.

But scale is itself a complication. Moving from a faculty position last year to chair of my department was a scalar shift; all of a sudden, I had obligations to a broad range of colleagues that I had to weigh in my own actions and statements. And I had much more direct engagement with people who were at different (higher?) scales: college- and university-level administration whose expectations for my performance came from different priorities and values. Even moving one step up the pyramid changed a great deal about the ways I think about and perform my job. Scale can carry with it a great deal of friction.

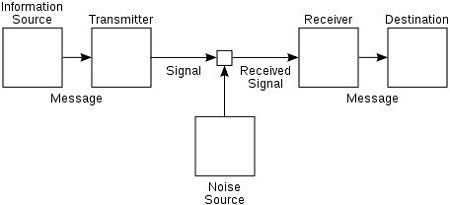

In some ways, then, this final installment of my post is about translation, and specifically how we translate across scales of activity. The word itself comes from Latin, and means something like “to carry across.” We typically use it to describe the process of moving from one language (or culture) to another, but it has more purchase than that. We tend to think of communication as the transmission of information or messages

when it’s probably more properly thought of as translation, with all of the challenges and difficulties that this activity entails. Noise is our baseline (and rhetoric the vitally important toolkit we all draw on to wrestle it into approximations of meaning).

So far, then, lurking behind these past couple of posts is a hypothesis about how, with respect to “the economy,” we’re witnessing a failure of translation. The signals being sent by the Biden administration aren’t being received. The solutions on offer—that the signal needs to be louder or that the receivers need a tune-up—don’t feel especially satisfying, and themselves ignore some of what I tried to get at in Part 2.

One of the larger issues, I think, is that the infrastructure for this messaging, opinion polls and media coverage, is showing its age. I talked a little in Part 1 about how survey design can affect outcomes, but even optimal survey design is limited by the shifts in technology during my lifetime. The turn from landlines to mobile has skewed pollsters’ ability to assemble representative samples1, and political polarization complicates this even further (even where it hasn’t similarly infected the pollsters themselves). The polled are more likely to answer performatively than accurately (see Michael Podhorzer on this). Like oversaturated advertising desperate to demonstrate its relevance, polling chases its audience in ways that compromise its accuracy (or usefulness), and the media struggles to put it in a reasonable context.

The same forces, writ larger, have wreaked havoc on the media. I grew up in the era where there were three television networks and a relatively stable ecosystem of local, regional, and national news via newspapers and magazines. It’s hard, I know, to imagine a time pre-internet, but communication channels were much slower and more concentrated. The shift to cable news and to the internet fragmented our attention, incentivized bad faith behavior, and irreversibly revalued the media. Tools that should have made it easier for us to inform our opinions about economics, politics, and society have largely done the opposite—linear improvements in access have produced exponential increases in noise and fog.

This particular story is my jam—not only did I live through these developments, but I spent no small part of my adult life first advocating for (some of) these changes, then watching media turn the corner into something empty and borderline disastrous. And unfortunately for our country, those shifts in infrastructure have made it difficult for any sort of leadership to emerge. This isn’t a Republican or a Democrat problem; it’s a gerontocrat problem. We’ve had far too many people in key positions of power whose media understanding basically stopped at the advent of CNN.

And the same can’t be said of corporate America, which has taken advantage not only of new technologies that government has been slow to understand/regulate, but they happened upon these shifts during the long winter of trickle-down jackassery2 that is, along with massive deregulation, one of the lasting legacies of the 80s. In our economies, as a result, the goal is less to make a living than to make a killing, and the extent to which various sectors have been monopolized is, I think, evidence of this. As Ed Zitron puts it in his piece on the Rot Economy, “Public and private investors, along with the markets themselves, have become entirely decoupled from the concept of what “good” business truly is, focusing on one metric — one truly noxious metric — over all else: growth.” In an actual free market, profits might be deployed in any number of ways: to improve one’s product, drop prices, invest in marketing—all of which might better one’s market share—or reward employees, improving their loyalty and commitment, etc. But those are “good business” options.

If your goal is to achieve a monopoly, the incentive to do any of these other things evaporates. Instead, you do things like stock buybacks, which Norfolk Southern embarked upon in lieu of tending to its abysmal safety standards, just prior to the disaster in Ohio. Or you actively make your products worse—the “enshittification” that Cory Doctorow writes about—because it’s the only way to squeeze higher profit margins from a market where there are no competitors. Or you use an outsized market share in one part of the cycle to wreak havoc on others’ as a way of undermining and annexing actual free markets, like Project Nessie at Amazon. Or you can pour those profits into lobbying efforts, so that you can campaign for worthy causes in public while undermining them in practice.

Or you can simply privatize, and bypass the scale-transparency tradeoff that emerged in the wake of the Great Depression, according to Rogé Karma. Karma explains that, over the past couple of decades, private equity has gone from a niche industry to controlling more than 20% of the economy, making it “effectively invisible to investors, the media, and regulators.” He writes,

This is not a recipe for corporate responsibility or economic stability. A private economy is one in which companies can more easily get away with wrongdoing and an economic crisis can take everyone by surprise. And to a startling degree, a private economy is what we already have.

We have a pretty clear example of the wrongdoing he refers to, but it’s being interpreted (by both sides) in political terms, rather than as a symptom of the long-festering rot that’s what actually “trickles down” to the rest of us. Without any sort of incentives (regulatory or otherwise) to behave responsibly, Zitron explains, “companies regularly do not function with the intent of making “good” businesses - they want businesses that semiotically align with what investors - private and public - believe to be “good.”” Speaking of pretty clear examples, that there are millions of people who still believe that, despite an extensive record indicating the contrary, a certain former President would be good for the economy. I’m not sure that I can think of another public figure whose semiotic alignment is so persistent.

Zitron’s notion of “semiotic alignment” is pretty crucial here—it’s another way of articulating the problem that prompted this post. Government messaging about the economy doesn’t semiotically align with many people’s lived experience, and we’re at a point culturally where we’re more likely to accuse the government of gaslighting (as one does on, say, TikTok or Reddit) than we are to take the time and effort to understand why things are out of joint.

Which is to say (and I think that this may inch towards a thesis statement on my part), our relationship to the economy is parasocial. Parasociality is an idea that’s been around for a long time (the term was coined in the 50s, but is much older in practice), and associated in particular with broadcast, screen media. The emergence of social media and the isolation imposed upon us by the pandemic have helped bring the term into common parlance. And platforms like YouTube, Twitch, and TikTok (and OnlyFans) have accelerated this, but American businesses caught on long before. (I’d probably locate my first exposure to it with Apple, whose products I’ve owned for more than 40 years now.)

By this, I don’t mean that we believe that the economy is our friend, but rather that we think of the major players in the economy that way. I’m cribbing here a bit from Wikipedia, which cites John Eighmey and Lola McCord’s 1998 study, "Adding Value in the Information Age: Uses and Gratifications of Sites on the World Wide Web," that argues that “the presence of parasocial relationships constituted an important determinant of website visitation rates. ‘It appears,’ the study states, ‘that websites projecting a strong sense of personality may also encourage the development of a kind of parasocial relationship with website visitors.’” (It’s no accident that this description holds true for political candidates and their voters, by the way.) We engage with the carefully crafted personae of economic actors (sometimes quite literally), and that “friendship” stands in for anything that might resemble actual knowledge (sometimes to the detriment of the corporation itself)

Those last two links come from Anne Helen Petersen’s work on Peloton, and as I was scanning back through them, a passage caught my eye:

A lot of people’s understanding of Peloton, its meaning, and its future has been fully alienated from the thing it actually produces, which is a pretty preposterously good workout that’s become a steady and often meaningful part of millions of people’s lives.

There’s a real loss there, I think. But it also helps explain the rot at the core of so many companies. If a product significantly changes the lives of its users, but only hundreds of thousands of them, not millions — it’s not legible as success. If a product doesn’t lean on the abject exploitation of those who make it, or the natural world whose resources compose it, thus lowering its profit margins — that’s not legible either. Not to the stock market, not to business press, and not, by extension, to the millions of people who passively absorb and understand information about the world around us.

This passage folds nicely with Zitron’s observations about the rot economy, I think. Legible success, Petersen writes, is blitzscaling, a term I’ve written about before. Petersen goes on to explain that “Success is billions, not millions. Success feeds on what Rebecca Solnit calls ‘the tyranny of the quantifiable.’” And there are only really a few who benefit from this, those folks at the very tiptop of the pyramid. The rest of us? We see folks like Jeff Bezos pulling in $13 billion in a single day, in the midst of a pandemic and a massive economic downturn, and rather than thinking about which circle of hell it is that permits this to happen, we wonder where our share is.

There’s a term in economics, homo economicus, that is “currently the most widespread model of human behaviour in economics.” It refers to the assumption, present in some economic theory, of “humans as agents who are consistently rational and narrowly self-interested, and who pursue their subjectively defined ends optimally.” Needless to say, there have been many criticisms of this approximation over the years, and this isn’t really a debate for which I have any particular insight or expertise. But it’s why I’ve titled this multi-part post the way I have, because I think that our veneration of wealth (and the people who hoard it) has a much broader economic effect than it should. FOMO (fear of missing out) is another of those ideas that’s entered our lexicon thanks to social media (and the creator economy), and I began this little journey into economics thinking that perhaps that was one of the things driving the difference between economic performance and public perception. Coming on the heels of COVID, which kept us from restaurants, movie theaters, concerts, and the like, the economy has only made our FOMO more acute.

And the consequence is what Kyla Scanlon has described recently as a “vibecession,” a condition “Where economically speaking, things are okay-ish but in reality… the vibes are off. People are feeling bad.”

If people have an experience (say, living through the 2008 recession) and evidence (home prices skyrocketing) that might shape some of their expectations - “wow, another unprecedented event to live through” which shapes their perception (things suck) and their interpretation of the future (things will continue to suck) - that shapes their narrative, which can shape reality.

Among other things (like several Republican devil-terms), one of the legacies of Karl Marx’s work was the idea that economies can be distinguished into base and superstructure. Base refers to the nuts-and-bolts of economies (markets, labor, institutions, policy), while superstructure rests atop it (think things like culture, religion, media, etc.). While they do impact one another, the traditional interpretation of this model is that the base is more determinant. In some ways, then, there’s a commonsense attitude towards the economy that what happens in the marketplace, banks, or the stock market is the real economy, while peoples’ feelings and social media posts are ephemeral, and ultimately inconsequential. Part of what Scanlon’s saying, and justifiably so, is that the superstructure matters far more than we might think; it’s why the “vibecession” can become a self-fulfilling prophecy. And while it’s by no means the only thing going on, it feels like the missing piece (or at least one of them?) to the semiotic alignment puzzle with which I began this post more than a week ago.

I began this installment by talking a little bit about translation, which I’d pose here as an alternative to the semiotic (mis)alignment that is typical of corporate and political propaganda. Thinking across scales requires translation, the ability to “carry across” a message even as we acknowledge that that movement shifts the message, that transposing it from one context to another is never without friction. And it’s more important than ever now to find sources that we trust to help with that process. We need translators. Over these three posts, I’ve cited many writers whom I’ve been reading for a while now, but I want to highlight a more recent one, Kyla Scanlon, in particular. I don’t know how I chanced upon her work, but it happened to be right at a time where I was thinking about this stuff, and in many ways, what modest virtues I’ve managed to achieve here are due in no small measure to her various channels. She pitches herself as someone who provides “human-centric economic analysis to help all of us understand the world better,” and I feel like she’s made me appreciably smarter in the past week or two. Her newsletter provides the transcripts, but her work is probably best digested on YouTube or TikTok. I also have her to thank for the occasional experience of thinking that I was saying something interesting, only to find a video from months ago where she said it first and better lol. This shallow dive of mine into economics was easier thanks to her as well, and I recommend her to you.

Time to skedaddle. I’ll leave you with a quick hit from the Doctorow piece I cited above, one that provides me with a bit of hope.

We used to put down rat poison and we didn’t have a rat problem. Then we stopped putting down rat poison and rats are eating us alive. That’s not a nice feeling, but at least we know at least one way of addressing it — we can start putting down poison again. That is, we can start enforcing the rules that we stopped enforcing, in living memory.

Of the things that the Biden Administration has done right, and there are a few, perhaps the best is the appointment of Lina Khan as chair of the FTC. Some of the best economic news we’re getting our of Washington these days has to do with the FTC’s willingness to take on some of the rats.

The “representative sample” is itself synecdochic, allowing the opinions of a couple of thousand people to stand in for millions

Not an economist! But I do realize that there’s a case to be made that trickle-down voodoo played an important role in bringing us out of the malaise of the 70s. But swinging the pendulum so hard in that direction also helped set the stage for regulatory capture, rising income inequality, and the widespread monopolization of various sectors that we live with today. I may very well be wrong about this, but rather than a course correction, that era was a hard-right turn that mistook “free markets” as “free from regularion” instead of “free to compete,” a misunderstanding that persists to this day.

Reading this, I wonder just how much of the translational breakdown has to do with an economy becoming only fiscal, or gov't backed, but no longer as fiduciary, or trusted/trustworthy—just a thought that is a subthread of recent grad class discussions about the attention economy Odell writes about. Granted, there are blurred edges among attention econ and fiscal econ, but as trust erodes, that fear of missing out can yield peace and occasional JOMO...or so you've gotten me thinking.