I am not an economist.

At the same time, economics is one of those fields where there’s a lot of lay understanding that circulates. It’s a discipline that most of us (myself included) think we understand far better than we do. I’m sure that, for anyone who’s spent time beyond the obligatory two-semester macro/micro sequence (unlike me), a lot of the popular discourse around our economy is as chafing as it is for me when I hear people tout Strunk and White as an exemplary text for learning to write.

Those people probably shouldn’t read this.

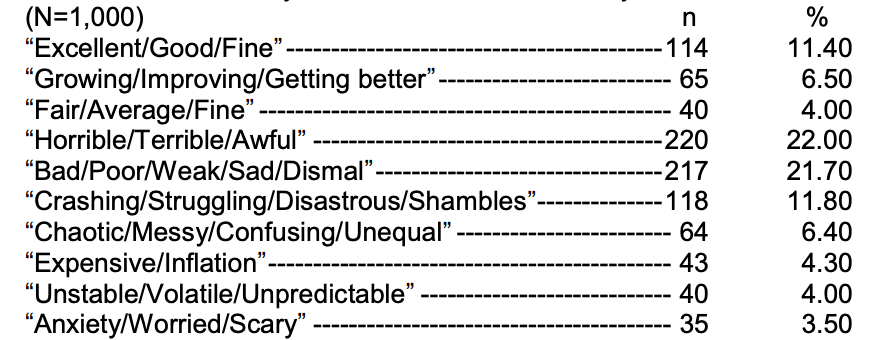

Anyway, this episode was prompted by a couple of recent polls that have been making their way across my feeds in recent weeks. The first is about a month old and comes from the Guardian; the story is titled “US economy going strong under Biden – Americans don’t believe it” and that offers a pretty solid explanation of what lies within. The Guardian poll came about a month after a Suffolk University poll that found that a significant number of Americans would trust TFG with the economy rather than Biden—you can see one write-up about this on The Hill.

I have to admit that it’s tempting for me to dig into these surveys. For example, it’s pretty well known that folks will often tend, with a spectrum of choices, towards the middle. So in the latter poll, given 10 choices, respondents clustered towards the middle 3 answers, all of which were synonyms for bad. (The choices offered were Good, Improving, Fair, and then 7 sets of those synonyms.) Whether this invalidates this question is (of course) debatable, but survey design can have an outsized impact on the conclusions, particularly when questions privilege a certain perspective.

But that’s not really what I want to talk about, although I may circle back to these surveys in a bit. Instead, I want to start with an overly bold statement, which is a little, but only a little, tongue-in-cheek:

There’s no such thing as the economy.

Like I said, this is a little bit facetious, but I’ll hedge in a couple of important ways. First, I’m not saying anything about economics, which I believe is an important field of study, one that generates a great deal of crucial knowledge about how our world works. But I’d be surprised if there weren’t folks in that field who insist on the fact that what they study isn’t “the economy” in any substantial way, but economies plural. “The economy,” in the way that it gets discussed in the media (and in the survey question above) is largely a myth, albeit a somewhat useful one and one that’s so commonly deployed as a shorthand that it’s entirely natural to us. But those surveys, and the recent media discussion of “Bidenomics” and “MAGAnomics,” have begun to curl the edges of that myth for me, to the point where I wanted to write about it this week.

As I mentioned, I don’t consider myself any sort of expert—if you asked me what I’d suggest we use in place of “the economy,” I’m not sure that I have a good answer. But I think that speaking about any economy above a certain size is problematic. When I think about the basic elements that compose economies—production, exchange, consumption, distribution—I tend to think first about personal and local economies. And honestly, taking just a step or two outwards in scale renders much of that entirely mysterious to me. For example, a single trip to the grocery store feels perfectly normal when I think about going to a place and paying a vendor money to receive a cartful of stuff. But that store is its own node in economies that are local, regional, and national, and each of those items in my cart represents an endpoint in a whole cycle of activity, similarly distributed across scales. Building an understanding of the economy from the ground up would be an impossible task—even a rough or cursory understanding of that single cart of groceries would probably take me weeks.

So we aggregate those details, and talk about different industries and markets, and organizations (like corporations) that operate at that scale. While these generalizations may not apply equally to every instance, there are virtues to that aggregation. A restaurant that is part of a national chain, for instance, has more margin for error than a local establishment, thanks to its membership in a broader economy. Cost of living calculators can be helpful tools for a quick glance understanding of the differences between two cities. (Scale is important here, for reasons that I probably won’t get to until Part 2.)

As we pull back even further, though, we begin to get closer to “the economy,” and as our perspective grows wider and more distant, we have to sacrifice all sorts of (potentially meaningful) detail. Every once in a while, I reflect upon the fact that I live only a few hours away from a city where the rent for a 1BR apartment, over the course of a year, would pay off several years of the mortgage I took out to buy my house. The median price of a house in my state is more than double what my own house is worth, so it’s fair to ask how valuable a statistic like that actually is, when there’s such a difference between local economies/markets. The answer, of course, is that it depends. It depends on the use to which you’re putting that information, as well as the range of data that’s being converted into an average or a median.

Another problem with “the economy” is that it unfolds unevenly and over time. If your lily pad is floating on the pond right next to where someone drops a bowling ball, the relationship between cause and effect is going to feel pretty instantaneous. But depending on the size of the pond, and where you’re at, it might take a long time for that ripple to reach you, if you even feel it at all. Let’s stick with real estate: in the late 2000s, the global recession that we experienced was triggered by the collapse of a housing bubble built upon the charmingly euphemistic phenomenon of “subprime mortgages.” I don’t want to get too deep into the weeds on this (especially not when Michael Lewis will do it for me), but while the attention of the country (and our leadership) was focused on the banks that primed and precipitated the crisis only to be bailed out later on, most of us probably paid little attention to all the houses themselves. While the bubble popped and all that money was lost, the properties themselves remained.

A couple of things have happened in the intervening fifteen years. Faced with a massive pool of depreciated assets, private equity firms began investing (more heavily?) in real estate, a trend that has continued to the present day. The NYT estimates that such firms have spent hundreds of millions in NYC alone—it’s hard not to imagine that the same hasn’t happened in major urban areas across the country. And their motives are not altruistic; they are looking for return on their investment, which means “rent increases and declining maintenance.”

But that less-than-ideal development may be the lesser of two evils. Because one of the other major housing trends is the emergence of services like AirBnB. A furnished space, left empty and leased to short-term visitors, can generate a great deal more revenue than a permanent tenant. I skimmed the local apartments available in my area on AirBnB, and there were plenty of 1BR places whose price, projected over a month, would cost me roughly the same as a month’s rent in NYC. Taking housing off the market to turn it into a “side hustle” is not only a viable path for many, but there are entire cable networks devoted to teaching us how to best to do it.

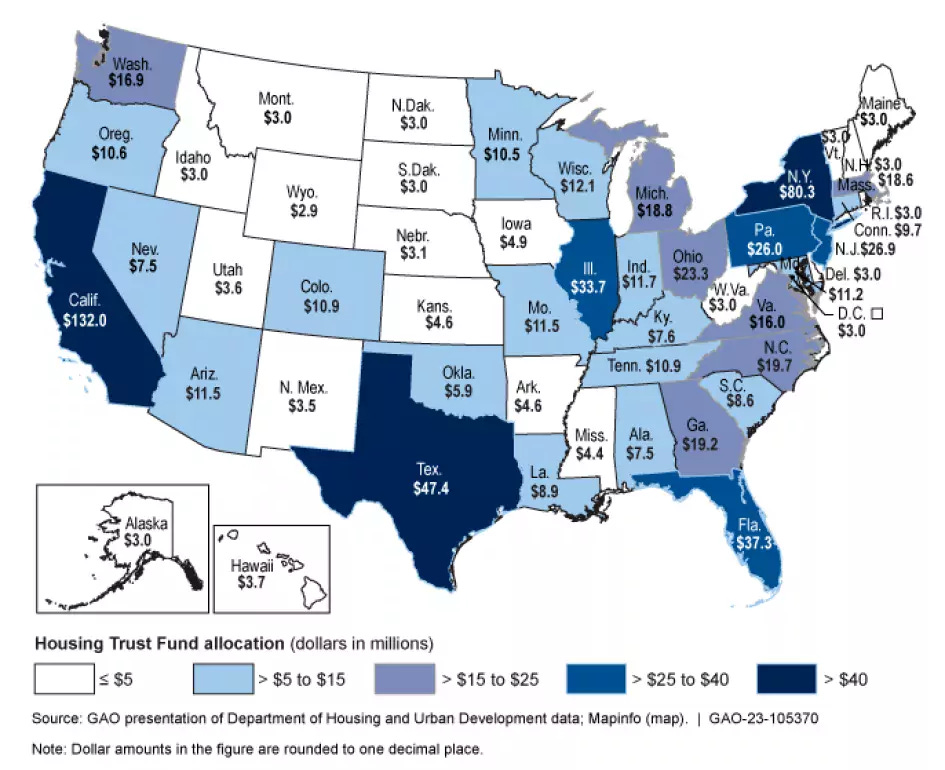

Given these trends, it’s small wonder that we hear so much negativity surrounding the issues of homelessness and housing affordability. But then, at the same time, “an estimated 420,000 new rental apartments were built in the United States, the highest amount for new multifamily construction in a half-century.” (It’s odd to find this info in an article about whether or not this construction is sufficiently stylish, but oh well.) On the one hand, this feels like a positive development, while on the other, increased supply of housing hasn’t really kept up as rent increased 24% over the past three years, according to the GAO.

Thinking about real estate and housing as a single, unitary phenomenon, and identifying trends like this, doesn’t really give us much beyond a statistical average, and that’s my point, I suppose. The map of HUD Housing Trust Fund allocation from that GAO link is instructive in this regard:

If we were to ignore state boundaries and drop it down to the level of region or city, I’d guess that the dark colors would thin out even further, and basically cluster around urban population centers. Those are the sites of the most housing, yes, but they’re also the sites where the most foreclosures occurred, and where AirBnB side hustles are likely to find the most value. They’re probably also the areas where a significant chunk of that new construction is located. Does this mean that there’s a national housing crisis? Honestly, I don’t know. The GAO and the media say so, but it’s pretty clearly uneven, and would require more than a single year’s data (or a single President’s term) to articulate, verify, and/or address.

And housing is one piece of a much larger picture, with a long, complicated history that folds in a number of other issues that I haven’t even discussed. I’m a fairly smart person, with better than average research skills, and even this piece of “the economy” is largely inscrutable for me.

When I was in graduate school, I read a great deal of French philosophy and literary theory. There was one book in particular that was exceptionally dense and complex, and about 2/3 of the way through, the author wrote directly to his audience, explaining that things were actually more complicated than they had seemed thus far. Whether or not he was poking fun at his reader, I do not know, but that sentence literally made me laugh out loud at the absurdity of it.

I feel like I’m at that point here, so I’m going to send this out, and move to part 2 (of a planned 3 parts). Part 1 here is about the fact that “the economy” is a myth, a veil we use to hide from ourselves the fact that economies are distributed and complicated, and difficult (if not impossible) to understand in any general, commonsense way. Part 2 is going to return to some (rhetorical) issues that I’ve been working through over the past few months, and argue that those issues are made visible by the surveys I mentioned above. If all goes well, Part 3 will be about what I’ve been trying to do to address both the limits of my own economic understanding and the rhetorical implications of an economy that’s mediated for us through news and social media.

And I will get around to explaining why I titled this post the way I did. It’ll just take me a while to get there.

And, when Bill Gates walks into a big-city Salvation Army soup supper, on average, everyone there is a millionaire.* Even here, in this out-of-the-way metro area, the number of cash sales of modest properties in the west end of cities on both sides of the river has increased significantly. I don't think that people who worked at, say, Tyson Meats, and who would've been over the moon to gain title to a 1,200 s.f. house with a yard, had suddenly come up with $150K in cash. It appears that it's something else here, too. But then, my model for home ownership was best described by George Bailey in trying to stave off a run on the Bailey Brothers' Building and Loan in that post-WWII movie about doing the decent thing. It strikes me that the "something else" we're getting here is more "Old Man Potter", and the wonderful life that Clarence would rescue us to will look a lot more like Potterville in this brave new world. Thanks for the points about survey design, too.

Tim L, Just up the Hill from Lock 15

*Also, if Mark Zuckerberg walked into the same soup supper, on average, everyone there would score as "a pretty decent guy" on the decent guy scale. Even him.